If you are buying or refinancing commercial property, you will likely hear the term ALTA Land Title Survey early in the process. Sometimes it comes from a lender. Other times it comes from a title company or an attorney. What makes this confusing is that not everyone agrees on when it is truly required. As a result, buyers often move forward thinking it is optional, only to face delays and pressure close to closing.

Why this question keeps coming up in real estate deals

At the beginning of a transaction, everything feels straightforward. Timelines look reasonable, and costs seem under control. However, due diligence becomes more serious as the deal moves forward. That is when survey requirements often surface.

Recently, surveyors have been more open about accuracy standards and responsibility. Because of this, buyers and investors have started asking smarter questions. One of the most common is not what an ALTA survey is, but who decides if it is required. That distinction matters more than most people realize.

Who actually has the power to require an ALTA Land Title Survey

Many buyers assume this decision belongs to them. In reality, the requirement usually comes from risk, not preference. Several parties can trigger it, often at different points in the deal.

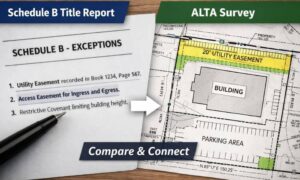

Title companies focus on what they are willing to insure. If they cannot confirm boundaries, access, or recorded rights with confidence, they limit coverage. When that happens, an ALTA Land Title Survey is often required to remove title exceptions. In short, the survey protects the policy just as much as it protects the property owner.

Lenders approach the issue differently. Early conversations may sound flexible, especially before paperwork is reviewed. However, once underwriting looks closely at the file, unclear access, shared improvements, or recorded easements often raise concerns. At that stage, lenders typically ask for more verification as part of the commercial due diligence process to make sure the property meets funding standards before approving the loan.

Attorneys look at long-term exposure. If there is a chance of future disputes, legal counsel may strongly recommend an ALTA survey even when others stay silent. Their priority is not speed. Instead, it is reducing liability after closing.

Buyers can sometimes decline an ALTA survey, but only in limited situations. This usually applies to cash purchases with no lender involved and limited title coverage. Even then, the buyer must knowingly accept the risk. Assumptions rarely hold up once the deal is complete.

When an ALTA Land Title Survey becomes required during due diligence

Timing plays a major role. The requirement almost never appears at the start of the deal.

During the letter of intent stage, surveys are rarely discussed in detail. Next, the title commitment is issued. This document lists recorded items and exceptions, which often raises the first questions. Then underwriting begins, and risk is reviewed more closely. This is when the requirement typically becomes formal.

By the time the deal reaches pre-closing, leverage is limited. If an ALTA survey is suddenly required at this stage, buyers often feel rushed. In reality, the conditions were building earlier. They just were not addressed.

When an ALTA Land Title Survey is truly optional

Despite common belief, an ALTA survey is not required in every transaction. Some deals allow flexibility.

Cash purchases may proceed without one, especially when the buyer accepts limited title coverage. Low-risk parcels with simple ownership history may not trigger concern. In some cases, a recent survey is accepted by all parties.

However, optional does not mean unnecessary. It simply means the risk stays with the buyer. Understanding that difference is critical. What is skipped during due diligence often shows up later, when fixing it costs more.

What happens when the requirement is ignored or misunderstood

Problems do not always appear right away. Often, they surface at the worst possible time.

Without an ALTA survey, title policies may include broad exceptions that limit protection. Lenders may delay funding until conditions are met. Buyers may lose negotiating power as deadlines approach.

After closing, unresolved issues can turn into disputes. Access questions, boundary conflicts, and easement problems rarely resolve themselves. When they appear later, solutions take longer and cost more.

How to avoid last-minute ALTA survey surprises

The best protection is clarity early in the deal. Ask direct questions before timelines tighten. Will the lender require expanded title coverage? Will the title company insure access without a survey? Who carries the risk if issues appear after closing?

Also, get answers in writing. Verbal guidance often changes once documents are reviewed. Written confirmation keeps everyone aligned and reduces stress later.

Most importantly, think in terms of risk transfer. Due diligence works best when every party understands who holds responsibility at each stage.

Final thoughts

Due diligence is not about checking boxes. It is about timing and risk. An ALTA Land Title Survey rarely becomes required by accident. It enters the process because someone needs certainty before moving forward.

Smart buyers do not wait to ask if they need one. Instead, they ask who might require it later and when that decision will happen. That approach saves time, money, and frustration.

In the end, the goal is simple. Close the deal with confidence, not surprises.